The rate of interest remains what it is, or stays taken care of, for the life of the car loan. Compare fixed-rate vs. adjustable-rate mortgages to see what's right for you. To learn about all your home-buying choices, have a look at these usual kinds of mortgage loans and whom they're fit for, so you can make the right option.

- While FHA lendings might appear attractive, it's important that you think about the overall cost of the funding when contrasting it to other alternatives.

- The amount you can obtain is partly based upon the amount of lease you anticipate to obtain yet loan providers will certainly take your income as well as personal conditions into account as well.

- By the end of the home mortgage term, thinking that you have actually made all of your repayments, you will certainly have paid off the original amount you borrowed, plus interest, as well as you will certainly own your home outright.

- This system was designed to help customers get 95% mortgages with a 5% deposit, with the government handling more of the risk as well as securing the loan provider.

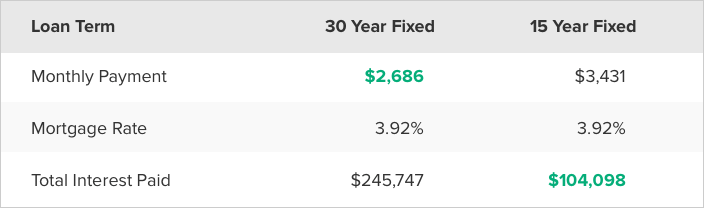

There are extra charges, though, including an upfront cost of 1 percent of the car loan amount and an annual cost. Fixed-rate loans are reduced threat over the term of the finance as well as offer even more certainty, although the first rate of interest tends to be higher. Variable-rate fundings can be an excellent option for people that understand they'll be moving prior to the introductory duration of their funding ends. Historically, concerning 75% of home customers select a fixed-rate lending, according to the Customer Financial Defense Bureau.

Examine the rates of interest you're paying and check out the small print before registering - there are typically better offers available when you take every little thing into account. An interest-only loan is a lending in which the consumer pays just the interest for some or every one of the term, with the principal equilibrium unchanged throughout the interest-only duration. This might be an attractive alternative for individuals that are stressed over their capital.

Whats A Guarantor Home Mortgage?

© 2022 NextAdvisor, LLC A Red Ventures Business All Legal Rights Reserved. Use this website makes up approval of our Terms of Usage, Personal Privacy Plan and also California Do Not Market My Individual Details. NextAdvisor might obtain compensation for some links to product or services on this site. An adjustable-rate mortgage might obtain you a lower rate of interest upfront, yet you have to be planned for that to go up gradually.

That Should Get A Big Loan?

These finances are best for those that know they can sell or refinance, or for those who can fairly expect to manage the greater monthly payment later on. With a variable-rate lending, also referred to as a variable-rate mortgage, your rate of interest might increase or down depending upon market problems. Adjustable-rate mortgages generally start with a reduced interest rate than a fixed-rate loan yet will alter after a particular number of years. If you choose a fixed-rate home loan, your rate https://canvas.instructure.com/eportfolios/1253043/edgarubws328/With_Home_Mortgage_Prices_Increasing_Arm_Fundings_Grabbing of interest is set when you get the funding and also Find more information won't change when rates of interest rise or down. This means your monthly repayments will stay steady for the life of the loan. The most usual sort of traditional loan, a fixed-rate lending suggests a solitary rate of interest-- and also regular monthly repayment-- for the life of the funding, which is usually can you sell a timeshare 15 or 30 years.

Pros Of Conventional Loans

Mortgage lenders typically calculate the amount of passion you are due to pay daily, monthly or annually. These kinds of mortgages typically fit having reduced down payments as well as have reduced application costs. A discounted home loan is supplied by lenders that intend to attract you to their a lot more expensive SVR by dropping their prices temporarily. The discount will be supplied for an introductory period-- normally between two as well as five years-- after which you'll be back on their more pricey home mortgage. Now that you understand the sorts of home mortgages, prevent the ones that'll cripple your monetary desires!

If you consider an ARM, it's important to check out the small print to recognize how much your price can enhance and also just how much you could end up paying after the initial period runs out. With a set price mortgage, as the name recommends, you pay a fixed interest rate for an established term, normally ranging from two to ten years, or in some cases also longer. This can supply important peace of mind, as your month-to-month home loan payments will coincide every month, no matter whether interest rates enhance on the broader market.